Key Takeaway

SR&ED rates are intact for 2026 — CCPCs still earn 35% refundable ITCs on the first $3 million — but documentation discipline is now the deciding factor in whether your claim survives a CRA review, especially for AI and ML work where scrutiny has measurably increased.

Every year, someone asks whether SR&ED is still worth claiming. The answer for 2026 is the same as last year: yes. The program is intact, the rates are unchanged, and Canadian companies doing genuine R&D should be filing.

That said, not everything is the same. CRA has increased scrutiny in specific areas, documentation expectations have tightened, and the government’s ongoing discussion about R&D incentive reform continues to generate noise worth filtering. This post separates the signal from the speculation.

What Has Not Changed

The program fundamentals are stable. Before getting into what’s different, it’s worth being clear about the baseline.

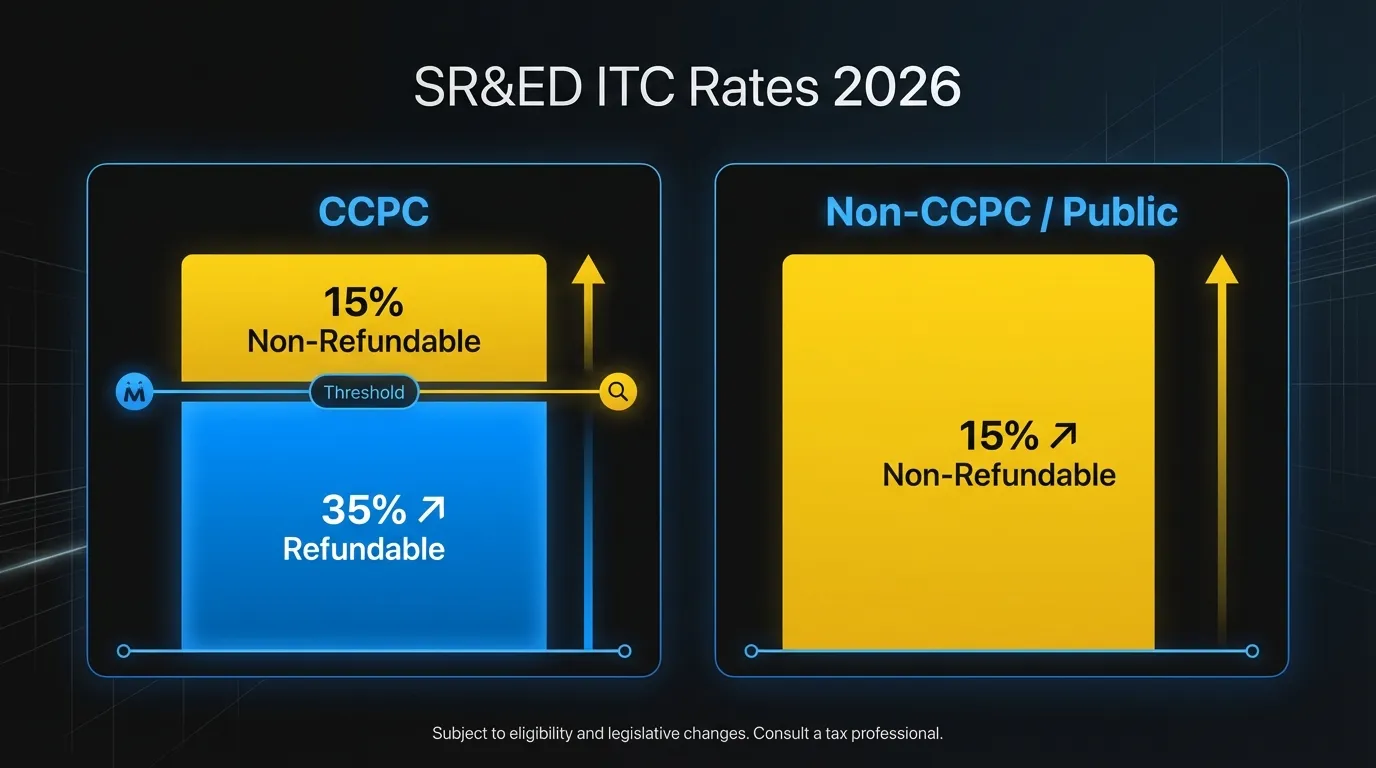

The investment tax credit rates are unchanged. Canadian-controlled private corporations (CCPCs) still earn a refundable ITC of 35% on the first $3 million of qualified SR&ED expenditures. Above that threshold, the rate is 15% (non-refundable). Non-CCPCs — public companies and large private companies — earn 15% non-refundable on all eligible spending.

The program eligibility criteria are unchanged. Work qualifies for SR&ED if it involves scientific or technological advancement, there’s technological uncertainty that couldn’t be resolved through standard practice, and the work is conducted through systematic investigation or search. CRA uses the same three-part test that has governed the program for decades.

The T661 filing process is unchanged. The form structure, the technical narrative requirements, and the filing mechanics are the same. If you filed last year, the process this year looks identical.

The filing deadline is unchanged. Corporations must file their SR&ED claim within 18 months of the tax year end in which the qualifying work occurred. This is a hard deadline. Missing it forfeits the claim. If your fiscal year ended in June 2025, your deadline is December 2026. See the full filing deadline guide.

What Has Changed

Is CRA reviewing AI and ML claims more carefully?

Yes. CRA’s Research and Technology Advisors (RTAs) are spending more time on software claims involving artificial intelligence and machine learning. This has been a documented trend since 2023, and it’s intensified.

The reason isn’t that AI work is presumed ineligible. It’s that this category has produced the highest rate of documentation problems and misapplied eligibility tests. Companies are claiming SR&ED for AI work that constitutes implementation of existing techniques, not investigation of technological uncertainty.

There’s a meaningful distinction between these two activities. Applying a published ML algorithm to a new dataset isn’t, on its own, SR&ED. Training a model using a known architecture to produce a known class of outputs isn’t, on its own, SR&ED. The eligibility question turns on whether you were investigating something that existing knowledge and standard practice couldn’t resolve — and whether you can document that investigation.

If your company is claiming SR&ED for AI or ML work in 2026, expect more scrutiny than in previous years. The documentation bar is higher — not because the eligibility criteria changed, but because CRA has seen enough poorly supported claims in this category to pay closer attention.

See what triggers a CRA audit and how to prepare.

Have documentation expectations changed?

Not in the rules, but in practice. CRA is consistently asking for more contemporaneous records — documentation created during the claim period, not reconstructed at filing time.

The T4088 guide (CRA’s technical guide to the T661) has been updated with additional clarifications on what constitutes acceptable documentation for project-level technical narratives. The updates don’t change eligibility requirements, but they clarify CRA’s expectations around specificity. Vague narratives about “investigating performance improvements” are less likely to survive review than specific descriptions of the technical uncertainty, the approaches tested, and the outcomes observed.

The practical implication: if your company assembles SR&ED documentation retroactively — asking engineers to write up their work at filing time rather than capturing it throughout the year — the risk of a documentation-based disallowance is higher than it was three years ago.

Does the Clean Technology ITC affect SR&ED planning?

For some companies, yes. Budget 2022 and Budget 2023 introduced a $1.7 billion Investment Tax Credit for clean technology. This program runs parallel to SR&ED and, for some companies, provides an alternative or complementary incentive for qualifying spending.

The Clean Technology ITC targets capital investments in clean energy, battery storage, and related manufacturing. It’s not a substitute for SR&ED, which remains focused on R&D expenditures (wages, contractor costs, materials). But companies working in clean tech who currently file SR&ED should know their expenditures may qualify for both programs under different eligibility criteria — and that their tax advisors may need to coordinate the treatment carefully.

This isn’t a reason to deprioritize SR&ED. For most Canadian software companies, SR&ED is the more accessible and more valuable incentive. The federal incentive landscape is broader than it was five years ago, and the planning considerations have become more involved for some companies.

What’s the status of SR&ED reform discussions?

No material changes have been enacted as of early 2026. The federal government has been signaling interest in modernizing Canada’s R&D incentive framework since at least Budget 2022. Multiple advisory bodies have raised concerns that SR&ED as currently designed underperforms compared to R&D incentives in other OECD countries, particularly for large corporations and deep tech investment. But these discussions haven’t produced legislation that alters the program fundamentals.

There’s no basis for reducing SR&ED claim activity based on anticipated program changes. The program exists, the rates are in place, and the government has consistently reaffirmed its commitment to supporting Canadian R&D investment.

What Does Heightened AI/ML Scrutiny Mean in Practice?

The core eligibility test for software SR&ED hasn’t changed. Work qualifies when you’re investigating technological uncertainty that can’t be resolved through standard practice or by looking up an answer in existing knowledge. What’s changed is that CRA’s reviewers now look more carefully at whether claims in the AI/ML space actually meet that standard.

CRA is distinguishing between two types of work:

Applying known techniques. You’re using a published ML framework, a known model architecture, and documented training approaches to achieve a result. The techniques are established. You’re doing engineering work to apply them. This isn’t SR&ED, regardless of how technically demanding the implementation is.

Investigating technological uncertainty. You’re encountering a problem that standard techniques don’t solve — perhaps because of a constraint specific to your data, your system architecture, or your performance requirements — and you’re conducting systematic experiments to find an approach that works. You can document what you tried, what failed, and what you learned. This is SR&ED.

The challenge is that most real AI development involves both activities in the same sprint. The work that qualifies is the investigation component, not the implementation component. Companies that can isolate and document the investigating work separately — rather than claiming all AI development as SR&ED — are in a stronger position.

This requires documentation practices that distinguish between the two categories of work as it happens. Reconstructing that distinction 18 months after the fact is much harder and produces documentation that’s less convincing to a reviewer.

How to document SR&ED claims properly under the T661 requirements.

What Should You Do Now?

The SR&ED program isn’t under threat. The rates are intact, the process is unchanged, and the government has repeatedly stated its commitment to the program. Companies doing genuine R&D should be filing.

What 2026 requires is documentation discipline, not program anxiety.

CRA is more likely to ask questions. When they do, the companies that come through reviews without adjustments are the ones that captured their qualifying work throughout the year, with specific project-level records that show the technological uncertainty they were investigating and the systematic approach they took.

The companies that face adjustments aren’t, in most cases, companies that over-claimed. They’re companies that did qualifying work and can’t document it clearly enough to survive review.

A few things worth doing now:

Audit your current documentation practices against what CRA actually expects. If your engineers are writing SR&ED narratives at filing time rather than capturing them during the year, that’s a gap worth closing before your next claim. The CRA’s updated T4088 guidance is specific enough that you can assess your current records against it directly.

For AI and ML work, document the distinction between investigation and implementation. Specifically: what was the technical uncertainty, what did you try, what did you observe, what did you change. If that documentation doesn’t exist in your current engineering workflow, it won’t be in your T661 narrative, and a 2026 review is more likely to surface that absence.

If you’re unsure what your current claim is worth or how it might hold up to review, the SR&ED calculator gives you a baseline estimate based on your actual R&D spending.

The deadline math matters too. If your fiscal year ends December 2025, you have until June 2027 to file. But the documentation for that period is being created right now. Waiting to think about SR&ED until Q4 next year means 12 months of qualifying work captured poorly — or not at all.

Frequently Asked Questions

Has the SR&ED program been cancelled or reduced for 2026?

No. The program is structurally unchanged. CCPCs still earn a 35% refundable ITC on the first $3 million of qualifying expenditures, with 15% non-refundable above that. The T661 filing process, eligibility criteria, and 18-month filing deadline are all unchanged. Reform discussions are ongoing, but no legislation has altered the program as of early 2026.

Does AI development qualify for SR&ED in 2026?

It can, but eligibility depends on the nature of the work. Applying published ML frameworks and known architectures to produce expected outputs doesn’t qualify. Work qualifies when you’re investigating a genuine technological uncertainty that standard techniques can’t resolve — and when you can document the systematic investigation, the approaches tested, and the outcomes observed. CRA is reviewing AI/ML claims more carefully in 2026, so documentation matters more than in prior years.

What documentation does CRA expect for AI and ML SR&ED claims?

CRA expects contemporaneous records — documentation created during the claim period, not reconstructed at filing time. For AI/ML work, this means project-level records showing the specific technological uncertainty, the experiments or approaches tested, the results observed, and what changed as a result. Commit histories, experiment logs, architecture decision records, and sprint retrospectives are all useful. The key is specificity: vague narratives about “performance investigation” won’t survive a 2026 review.

Ready to strengthen your SR&ED documentation? Chrono R&D connects to your development tools, captures qualifying work automatically, and produces CRA-ready documentation throughout the year. Talk to us about your SR&ED claim.