Key Takeaway

Companies that integrate SR&ED into multi-year financial planning recover 85-95% of eligible credits, while reactive filers capture barely half.

SR&ED claims happen once a year. The strategy behind them shouldn’t.

Most Canadian software companies approach SR&ED reactively. The fiscal year ends, someone remembers to file, and a consultant scrambles to reconstruct what the engineering team worked on twelve months ago. That approach captures some credits. It leaves a significant amount unrecovered.

Companies that treat SR&ED as a continuous financial planning tool recover substantially more. They align their claim strategy with hiring plans, funding rounds, product pivots, and corporate tax positioning. Over a three-to-five year horizon, the difference compounds into hundreds of thousands of dollars.

How Does Company Stage Change the SR&ED Math?

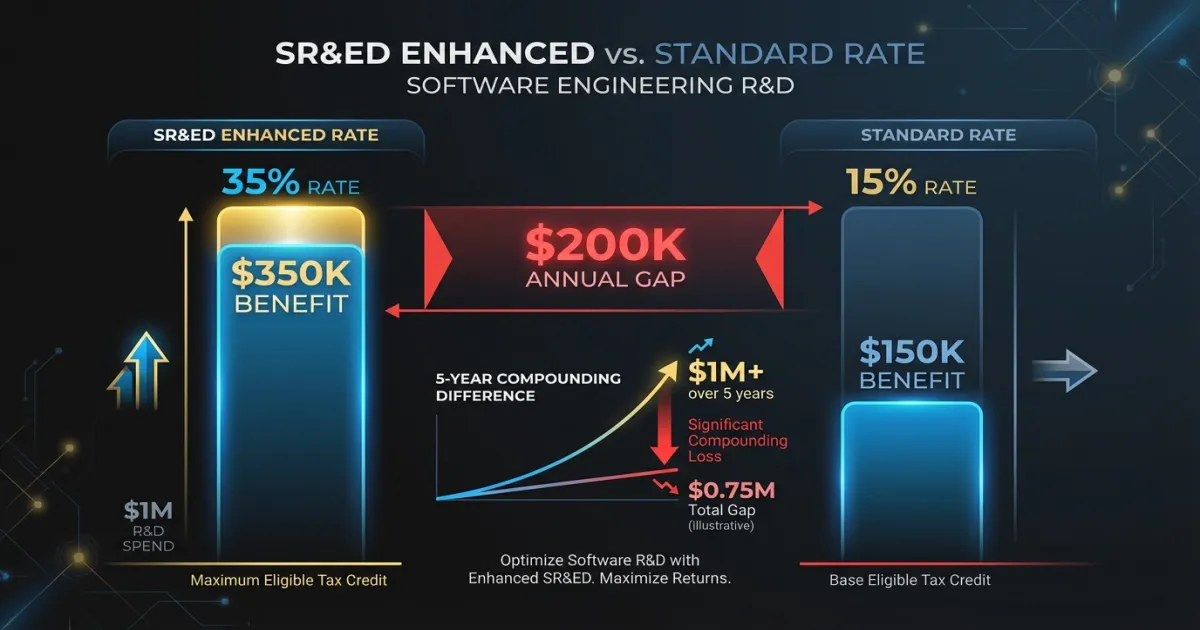

The single most important variable in SR&ED planning is your corporation’s status and income level. It determines your Investment Tax Credit (ITC) rate.

Canadian-controlled private corporations (CCPCs) with taxable income under $500,000 and taxable capital under $10 million qualify for the enhanced ITC rate: 35% of qualifying SR&ED expenditures. The credit is fully refundable. You get a cheque from CRA even if you owe zero corporate tax.

Once you cross those thresholds, the rate drops to 15%, and the credit becomes non-refundable. It can only offset taxes payable.

This isn’t a minor difference. A company spending $1M per year on qualifying R&D gets $350,000 back at the enhanced rate versus $150,000 at the standard rate. That’s a $200,000 annual gap.

For early-stage startups, this usually isn’t a concern. Pre-revenue companies sit comfortably below the thresholds. But fast-growing companies need to watch the transition. The year your taxable income crosses $500K is a financial planning event. Knowing it’s coming lets you time R&D investments, bonus structures, and other deductible expenses to stay below the threshold for as long as it’s legally and strategically sensible.

Your accountant should model this transition at least two fiscal years in advance.

How Do Funding Rounds Affect SR&ED Timing?

Venture-backed companies have an unusual relationship with SR&ED. The credits represent non-dilutive capital, which makes them attractive for the same reason grants are: they fund operations without giving up equity.

Timing matters. If you’re raising a Series A and expecting a $300,000 SR&ED refund within six months, that refund effectively extends your runway without adding to the round size. Some founders raise slightly less equity because the SR&ED refund covers the gap. Others time their filing to have the refund arrive between rounds, reducing the pressure to raise at an unfavorable valuation.

If your refund won’t arrive fast enough, SR&ED financing lets you borrow against the expected credit. Lenders advance 60-80% of the expected refund value, with the CRA payment going directly to the lender when it arrives.

The strategic question for founders: would you rather dilute 2% more on your next round, or file a strong SR&ED claim that covers the same dollars? For a company spending $800K per year on qualifying R&D at the enhanced rate, that’s $280,000 in refundable credits. That’s meaningful dilution avoided.

One nuance worth flagging: the tax treatment of SR&ED refunds affects how credits interact with your financial statements and investor reporting. Get your controller aligned on this before the board meeting.

Why Does Team Scaling Change What You Can Capture?

A five-person engineering team and a fifty-person engineering team generate very different SR&ED claims.

The obvious reason: more engineers means more qualifying salary expenditures. If half your engineering team’s time goes toward work involving technological uncertainty, growing from 10 to 40 engineers roughly quadruples your eligible expenditure base.

The less obvious reason: larger teams create more qualifying projects. A small team might run two or three projects that involve genuine technological uncertainty per year. A team of forty, organized across multiple squads, might run ten to fifteen. Each project is a separate SR&ED claim line with its own technical narrative.

The documentation challenge scales with team size. Five engineers can sit in a room and reconstruct a year’s worth of technical decisions. Forty engineers across eight squads cannot. By the time you’re at twenty-plus developers, you need a systematic capture process running throughout the year, not a retrospective scramble during filing season.

Plan your SR&ED documentation process alongside your hiring plan. If you’re going from 10 to 30 engineers over the next eighteen months, Q1 of that growth period is when you set up the tooling and workflows to capture qualifying work continuously. Waiting until you’ve already scaled means you’ll lose the first year of expanded claims to poor documentation.

How Do Product Pivots Open New SR&ED Claims?

Companies that change strategic direction often assume their SR&ED story gets weaker. The opposite is usually true.

Each new technical direction introduces fresh technological uncertainty. When your team pivots from a monolithic architecture to a microservices approach, the investigation into how to decompose, migrate, and maintain the new system is textbook SR&ED material. When you abandon a machine learning approach that wasn’t performing and explore a fundamentally different technique, the systematic work on both the failed and the replacement approach can qualify.

Failed experiments from abandoned product lines are still eligible. CRA evaluates whether the work met the three-part test (technological uncertainty, systematic investigation, technological advancement) at the time it was performed. The fact that you later decided not to ship the product is irrelevant to the claim.

This is where companies most frequently under-claim. There’s a natural instinct to avoid drawing attention to work that “didn’t go anywhere.” But a six-month investigation into a distributed caching architecture that you ultimately replaced with a different approach generated real technical knowledge. That work qualifies, and it represents real salary expenditure that you can recover. Check our SR&ED examples library for real-world cases.

Don’t let pivot shame cost you money.

What Are the ITC Carry-Forward Rules?

Not every company can use SR&ED credits immediately. Pre-revenue startups with no taxable income and companies in a loss position may generate non-refundable ITCs they can’t apply right away.

The carry-forward rules are generous. Unused ITCs can carry forward 20 years or back 3 years. If you’re generating non-refundable credits today because you’ve crossed the CCPC thresholds but don’t have enough taxes payable to absorb them, those credits sit on your balance sheet as a future tax asset.

This changes the math on R&D investment timing. A company that expects to become profitable in year three can invest aggressively in R&D during years one and two, accumulate ITCs, and then apply them against taxes payable once revenue catches up. The effective cost of that early R&D drops significantly when you account for the credits you’ll eventually use.

For companies evaluating whether SR&ED is a grant or a credit, the carry-forward mechanism is one of the key distinctions. Grants are one-time. SR&ED credits accumulate and compound.

Pre-revenue companies should still file claims every year, even if the immediate refund is small or zero. Establishing a consistent filing history with CRA strengthens future claims, and the carried-forward ITCs have real financial value that shows up when you reach profitability.

How Does SR&ED Reduce Your Burn Rate?

For startups, the most intuitive way to think about SR&ED is as a reduction in R&D burn rate.

A CCPC at the enhanced rate recovers 35% of qualifying SR&ED expenditures. If your monthly engineering payroll is $200,000, and 60% of that time involves qualifying work, you’re generating $42,000 per month in SR&ED credits. That’s $504,000 per year.

Over three years of consistent claiming, that’s $1.5M in recovered capital. At a monthly burn rate of $350,000, that’s more than four months of extended runway.

The SR&ED calculator can give you a specific estimate based on your expenditure profile. Run the numbers before your next board meeting. The gap between “we should look into SR&ED” and “we’ve been claiming for three years” is often the difference between raising a bridge round and not needing one.

Even at the standard 15% rate, a company spending $2M per year on qualifying R&D recovers $300,000 annually. Over five years, that’s $1.5M in credits against taxes payable.

What Does an Annual SR&ED Planning Cycle Look Like?

The companies that capture the most don’t treat SR&ED as a separate process. They integrate it into their existing financial planning cadence.

Q1: Review and file the prior year. Your fiscal year just ended. Within six months of your year-end, compile the technical narratives, calculate eligible expenditures, and file the T661 with your T2 corporate tax return. If you’ve been capturing documentation throughout the year, this takes weeks. If you haven’t, it takes months and you’ll miss things.

Q2: Mid-year assessment. Six months into the current fiscal year, review what the engineering team has been working on. Identify projects that involve technological uncertainty. Flag work that’s at risk of being under-documented. This is the checkpoint where you course-correct before it’s too late.

Q3: Capture and document. The bulk of the documentation effort should happen close to when the work occurs. Engineers write better technical narratives about problems they solved last month than problems they solved eleven months ago. If you’re using automated capture tools like Chrono R&D, verify they’re pulling the right data. If you’re relying on manual documentation, schedule it now.

Q4: Pre-assessment and next-year strategy. Before the fiscal year ends, estimate the current year’s claim size. Review planned R&D initiatives for the coming year. Identify projects likely to involve qualifying uncertainty. Adjust documentation workflows if the team has grown. Align with your accountant on ITC utilization strategy, carry-forward positions, and any threshold transitions on the horizon.

This cycle takes approximately 20 hours per quarter for a finance lead to manage, assuming the documentation capture is running continuously. That’s a modest investment for what is typically the largest non-dilutive capital source available to Canadian software companies.

What’s the Real Cost of Reactive SR&ED Filing?

The gap between a reactive SR&ED approach and a strategic one grows wider every year. A company that files inconsistently and documents poorly might recover 40-60% of what they’re entitled to. A company running a disciplined multi-year strategy recovers 85-95%.

On a $500,000 annual claim, the difference between 50% and 90% recovery is $200,000 per year. Over five years, that’s $1M left on the table.

The starting point is straightforward: calculate what you’re eligible for today, establish the documentation process, and integrate SR&ED into your financial planning cycle. The credits compound. The documentation habit gets easier. Three years from now, you’ll have recovered capital that funded real growth without diluting a single share.

FAQ

Can I file SR&ED retroactively for years I missed?

You can file an SR&ED claim up to 18 months after your fiscal year-end. Beyond that window, the claim is gone. If you missed prior years, there’s no way to recover those credits. The best time to start was three years ago. The second best time is your current fiscal year.

How much does a multi-year SR&ED strategy cost to maintain?

About 20 hours per quarter for a finance or operations lead, assuming you use automated documentation tools. The main cost is establishing the process in year one. After that, the cycle runs on its own. For context, a $500,000 annual claim at 90% recovery returns $450,000. The time investment pays for itself many times over.

Does switching SR&ED consultants or tools reset my claim history?

No. Your SR&ED filing history belongs to your corporation, not your consultant. CRA tracks claims by business number. Switching providers doesn’t affect your track record or carry-forward positions. If anything, a better process improves your standing with CRA over time.

Ready to build a multi-year SR&ED strategy? Talk to our team. We help Canadian software companies structure claims that compound year over year.