Key Takeaway

Contractor payments qualify for SR&ED at 80% for arm's-length relationships, but only when your team directs the R&D and the work happens in Canada.

Canadian software companies don’t build products with a single, fully employed team anymore. Contractors, freelancers, agencies, and offshore developers show up in almost every engineering org. That mixed workforce creates a set of SR&ED rules most companies either ignore or get wrong.

Some companies exclude all contractor work from their claims. Others include everything and hope CRA doesn’t look closely. Both approaches cost money. The first leaves legitimate credits unclaimed. The second invites reassessment.

CRA has specific, well-documented rules for how contractor and outsourced development fits into an SR&ED claim. The rules change depending on the contractor relationship, who directs the work, and where it gets done.

How Does CRA Classify Contractor Relationships?

Before anything else, CRA classifies every contractor relationship as either arm’s-length or non-arm’s-length. The classification determines how much of the payment you can claim.

Arm’s-length means the two parties operate independently. No controlling interest, no family relationship, no shared ownership. Most freelancers, agencies, and outsourced development firms are arm’s-length to the claimant.

Non-arm’s-length means the parties are related. A subsidiary, a company owned by the same founder, a contractor who is also a shareholder. CRA applies the Income Tax Act definition here, which includes related persons, persons connected by common control, and certain trust relationships.

The distinction matters because of how each category gets claimed.

For non-arm’s-length contractors, you claim the contractor’s actual SR&ED expenditures, not the amount you paid them. If you paid a related company $200,000 but their qualifying salary and materials costs were $120,000, you claim $120,000. The markup doesn’t count.

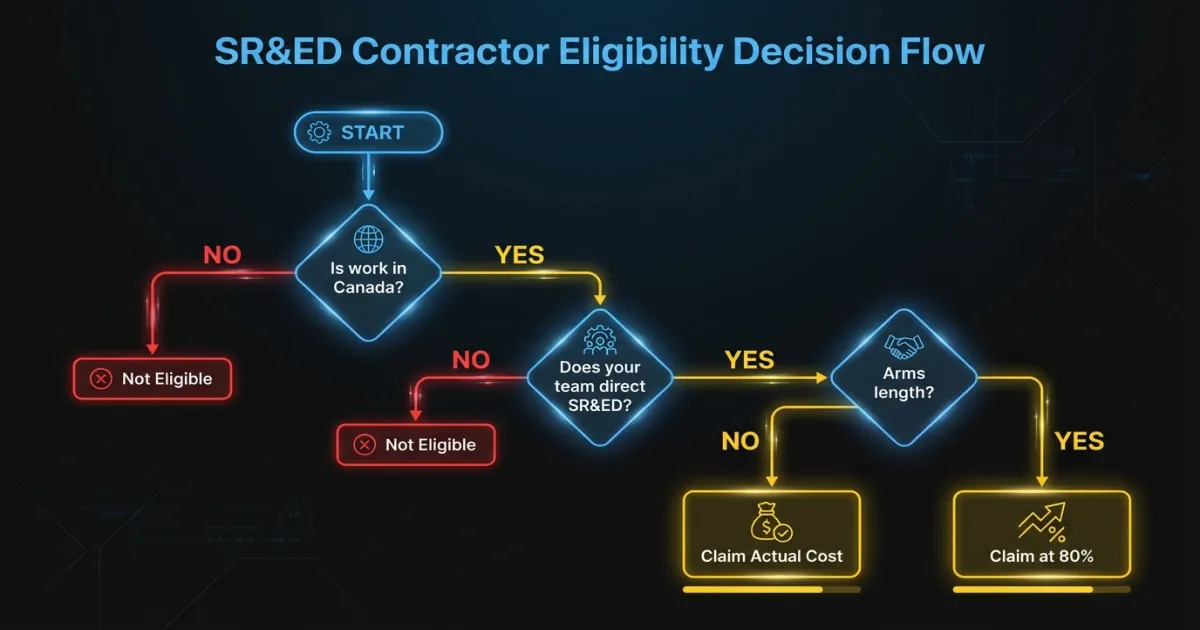

For arm’s-length contractors, you claim based on the payment amount. But only 80% of it.

What Is the 80% Rule for Arm’s-Length Contractors?

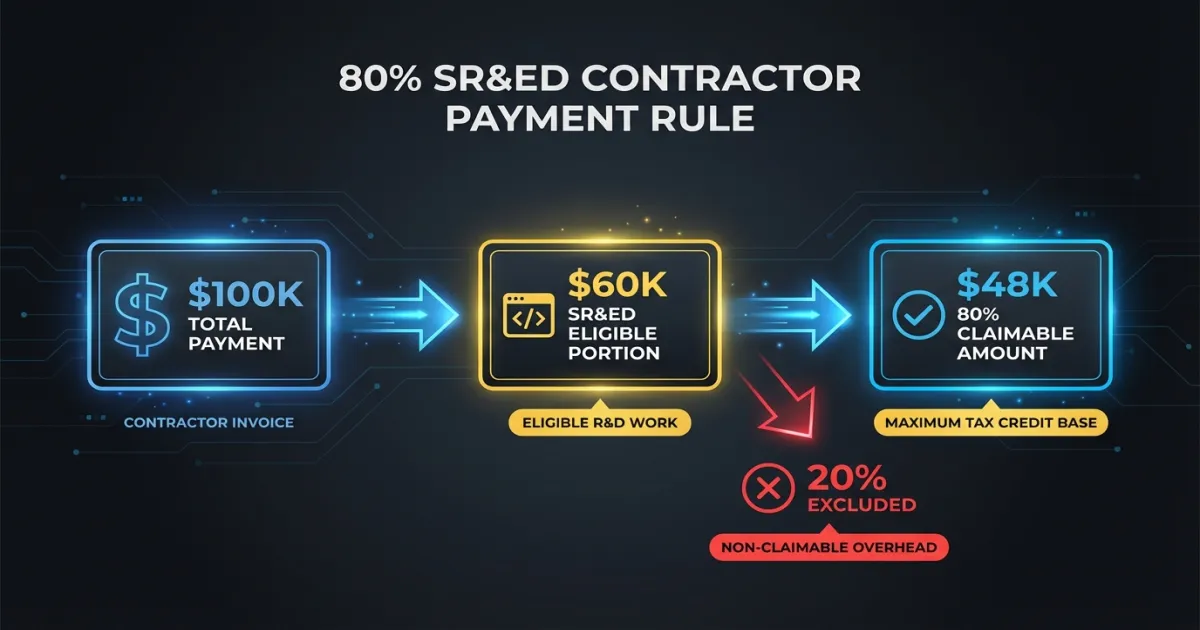

When you pay an arm’s-length contractor to perform SR&ED work, CRA allows you to include 80% of the payment as an SR&ED expenditure. The remaining 20% is excluded.

The math is straightforward. If you paid a development agency $100,000 for work that qualifies as SR&ED, you include $80,000 in your claim. The 80% cap applies to the total payment for qualifying work, not to the entire contract value. If only half the contracted work was SR&ED-eligible, you apply the 80% to the eligible portion.

| Payment to Arm’s-Length Contractor | SR&ED-Eligible Portion | Claimable Amount (80%) |

|---|---|---|

| $50,000 | $50,000 (100%) | $40,000 |

| $100,000 | $60,000 (60%) | $48,000 |

| $200,000 | $150,000 (75%) | $120,000 |

The 80% rule exists because CRA assumes a portion of any arm’s-length payment covers the contractor’s profit margin. CRA doesn’t consider that margin an SR&ED expenditure. Whether the actual margin is 5% or 40%, the flat 80% applies.

One common mistake: companies sometimes apply the 80% to the full contract value rather than isolating the SR&ED-eligible portion first. This inflates the claim and creates problems during review.

What’s the Difference Between “For” and “On Behalf Of”?

This distinction determines whether contractor payments qualify at all. CRA draws a hard line between work performed “for” the claimant and work performed “on behalf of” the claimant.

Work performed “for” the claimant means the contractor carries out SR&ED under the claimant’s direction and control. The claimant defines the technological objectives, supervises the investigation, and retains the intellectual property. The contractor executes work within a framework the claimant controls.

Work performed “on behalf of” the claimant means the contractor independently performs SR&ED and delivers results. The claimant specifies what they want built. The contractor decides how to solve the technological problems and directs the investigation.

Only payments for work performed “for” the claimant qualify as SR&ED contract expenditures under the traditional filing method. If the contractor performs SR&ED “on behalf of” the claimant, the contractor themselves can make the SR&ED claim. The claimant cannot.

This is where many companies get tripped up. When you hire an agency and say “build us a recommendation engine that can handle 10 million users,” the agency’s internal R&D to solve that problem is likely being performed “on behalf of” you. You specified the outcome. They directed the investigation. That work belongs to their SR&ED claim, not yours.

Compare that to bringing a contractor into your team, assigning them to a specific technological uncertainty your engineers identified, directing the experimental approach, and reviewing results alongside your team. That contractor is performing work “for” you.

The practical test CRA applies: who had supervision and control over the SR&ED activities? Not the project. The SR&ED activities specifically.

How Does CRA Evaluate Supervision and Control?

CRA evaluates supervision and control by looking at several factors:

Who identified the technological uncertainty? If your team defined the problem and the contractor is helping solve it under your direction, that points to “for” the claimant.

Who designed the experimental approach? The party that decided which hypotheses to test and what methods to use typically has control over the SR&ED.

Who reviewed and interpreted results? If your engineers reviewed the contractor’s work, decided what to try next based on failed experiments, and directed subsequent iterations, that supports your claim.

Who retained the IP? IP ownership alone doesn’t determine the classification, but it’s a supporting factor CRA considers alongside the others.

What did the contract say? CRA looks at the written agreement. If the contract specifies deliverables and leaves the method to the contractor, that suggests “on behalf of.” If it specifies the technical work to be performed under the claimant’s direction, that supports “for.”

This test applies to every contractor engagement you include in an SR&ED claim. Document the answers to these questions before filing. During a CRA review or audit, these are exactly the questions the reviewer will ask.

Does Offshore Development Qualify for SR&ED?

This is where many Canadian companies lose eligibility entirely. SR&ED expenditures must relate to work performed in Canada. The geographic requirement is strict.

If you have developers in India, Ukraine, the Philippines, or anywhere outside Canada performing the R&D work, those payments don’t qualify as SR&ED expenditures. It doesn’t matter that the Canadian company directs the work, that the IP is owned in Canada, or that the contractor is paid through a Canadian entity.

The work itself must be performed on Canadian soil.

CRA allows limited exceptions. SR&ED work performed outside Canada can qualify if it was done to achieve the objectives of related SR&ED carried on in Canada, and the work could not reasonably have been performed in Canada. Both conditions must be met. In practice, this exception is narrow. “Our offshore team was cheaper” isn’t a valid reason. “The only lab with this specific testing equipment is in Germany” might be.

For companies with distributed teams, this means carefully tracking which development work was done by which team members in which locations. A developer working from Toronto on a qualifying project generates claimable expenditures. The same developer working from Lisbon on the same project does not.

What About Mixed Teams With Canadian and Offshore Developers?

Many Canadian software companies have a structure like this: 5-10 developers in Canada, 15-30 developers offshore. The Canadian team leads architecture and design. The offshore team handles implementation.

In this structure, the eligible SR&ED activities are limited to the work performed by the Canadian team. If the Canadian team identifies a technological uncertainty, designs experiments, and evaluates results, that work qualifies. The offshore team’s implementation of those experiments, even under Canadian direction, doesn’t qualify because of the geographic restriction.

This is a common source of under-claiming. Companies assume that because the offshore work doesn’t qualify, none of the work qualifies. The Canadian team’s contributions are still eligible. Separate the work by location and claim the Canadian portion.

How Should You Structure Contracts for SR&ED Eligibility?

The contract language between you and your contractors affects your SR&ED claim. CRA reviews these agreements during audits. Contracts drafted without SR&ED in mind often use language that inadvertently disqualifies the work.

What Your Contracts Should Include

A clear statement of direction and control. The contract should specify that the claimant directs the SR&ED activities, defines the technological objectives, and supervises the experimental work.

Separation of SR&ED and non-SR&ED work. If a contractor performs both qualifying and non-qualifying work, the contract should distinguish the two. Ideally with separate line items or statements of work.

Work location requirements. If geographic eligibility matters (and it almost always does), the contract should specify that the SR&ED work will be performed in Canada.

IP assignment clauses. While IP ownership alone doesn’t determine eligibility, having IP assigned to the claimant supports the “for” classification.

Record-keeping obligations. The contract should require the contractor to maintain contemporaneous records of their SR&ED activities, including time tracking by project, technical notes, and experimental results.

What to Avoid

Contracts that describe only deliverables with no reference to the technical investigation process. These read as “on behalf of” arrangements to CRA.

Lump-sum contracts with no breakdown between qualifying and non-qualifying work. CRA will challenge your allocation if you can’t support it with contract terms.

Contracts that give the contractor full discretion over the technical approach. This undermines the supervision and control argument.

What Documentation Does CRA Expect for Contractor SR&ED?

The documentation standard for contractor work is higher than for in-house work. CRA expects you to demonstrate not just that the work was SR&ED, but that you directed it.

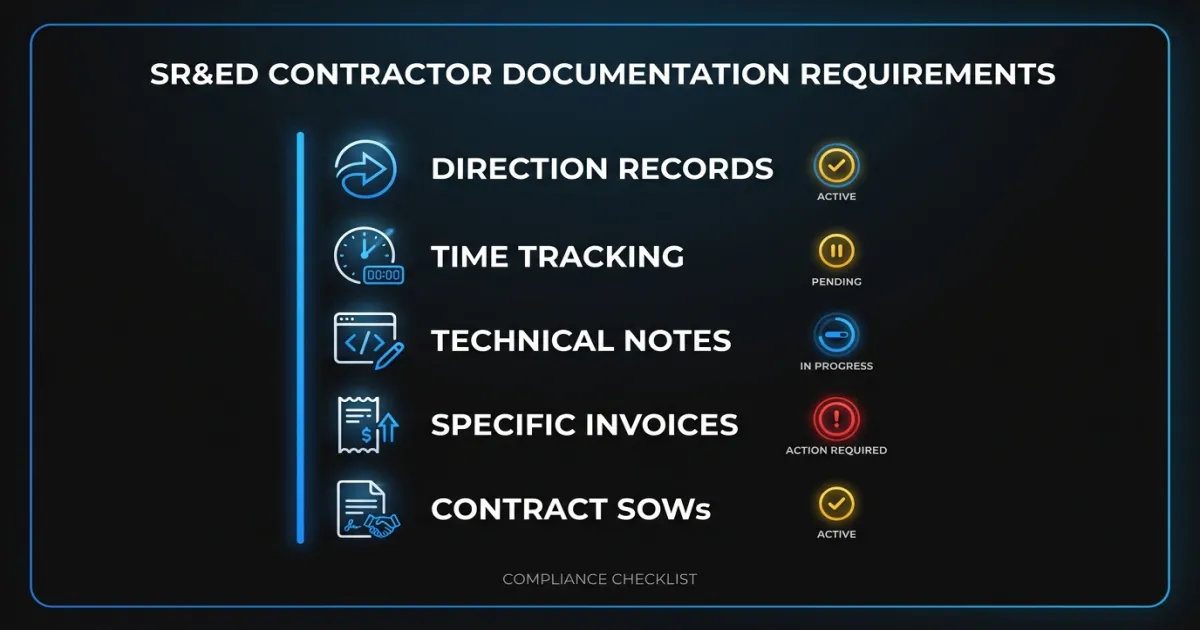

Contemporaneous records of direction. Emails, Slack messages, meeting notes, or Jira tickets showing that your team defined the technical objectives and directed the experimental approach. “Contemporaneous” means created at the time, not reconstructed later.

Time tracking by project and activity. The contractor’s hours should be broken down by project, with SR&ED-eligible activities separated from routine development. This is essential for calculating the eligible portion of their payments.

Technical progress notes. Regular documentation of what was attempted, what failed, what was learned, and what changed as a result. This maps to the technical narrative requirements for describing the systematic investigation.

Invoices that reference specific work. Generic invoices (“development services, March 2026”) are weak. Invoices that reference specific projects or work packages, matched to your internal records, are much stronger.

Contract amendments and SOWs. If the scope of work changed during the engagement, documented amendments showing how SR&ED activities evolved support your claim’s narrative.

The real cost of poor process isn’t consultant fees. It’s lost credits from contractor work that qualified but was never properly documented.

What Are the Most Common Contractor SR&ED Mistakes?

Excluding all contractor work from the claim. This is the most expensive mistake. If contractors performed qualifying SR&ED under your direction in Canada, those payments (at 80% for arm’s-length) belong in your claim.

Including contractor work without establishing direction and control. If CRA determines the contractor performed SR&ED “on behalf of” you rather than “for” you, the entire contractor portion of your claim gets denied. Not reduced. Denied.

Failing to prorate for mixed work. Contractors rarely spend 100% of their time on SR&ED-eligible activities. Apply the eligible percentage before the 80% rule, not after. And have documentation to support your allocation.

Ignoring the geographic requirement. Paying a Canadian entity that subcontracts to offshore developers doesn’t make the work Canadian. CRA looks at where the work was physically performed.

Reconstructing documentation after the fact. CRA auditors can distinguish contemporaneous records from documents created during claim preparation. Build documentation into your workflow from the start, not at year-end.

How Do You Get Started With Contractor SR&ED Claims?

The rules around contractor SR&ED are specific but not complicated once you map them to your actual team structure. Start with three questions:

- Which contractors are performing work that meets the SR&ED eligibility criteria?

- For each qualifying engagement, does your team direct and control the SR&ED activities?

- Is the work performed in Canada?

If the answer to all three is yes, those contractor payments belong in your claim at 80% (arm’s-length) or at actual SR&ED cost (non-arm’s-length).

If you have a mixed team with both Canadian and offshore contributors, segment the work by location and claim the Canadian portion. Don’t let the complexity of a distributed team stop you from claiming work that legitimately qualifies.

Companies that get this right build SR&ED tracking into their contractor management process from day one. They structure contracts with eligibility in mind, require time tracking that separates qualifying work, and maintain direction-and-control records as part of normal project management. Filing then becomes compiling existing records rather than reconstructing a year’s worth of contractor activities.

FAQ

Can I claim SR&ED for work done by freelancers or agencies?

Yes, if three conditions are met: the work qualifies as SR&ED under CRA’s eligibility criteria, your team directed and controlled the SR&ED activities (the “for” test), and the work was performed in Canada. Arm’s-length contractor payments are claimable at 80% of the eligible portion.

Does offshore development ever qualify for SR&ED?

Almost never. CRA requires SR&ED work to be performed in Canada. The only exception is when the work was necessary to achieve objectives of Canadian-based SR&ED and could not reasonably have been done in Canada. In practice, this exception is very narrow.

What happens if CRA determines our contractor work was “on behalf of” rather than “for” us?

The entire contractor portion of your claim gets denied. CRA doesn’t reduce it. They remove it. To avoid this, structure contracts with clear direction-and-control language, maintain contemporaneous records of your team supervising the SR&ED activities, and document who identified the technological uncertainty and who designed the experimental approach.

Not sure whether your contractor arrangements qualify for SR&ED? Talk to our team. We help Canadian software companies structure contractor claims that hold up under CRA review, with documentation that proves direction and control from day one.